Most people who have known me for the last 10 or so years knows I have a deep respect for the initial intent of cryptocurrency. You can read about it on this site, in fact. This, however, is not a story of cryptocurrency. It’s a story of fraud perpetrated by some of the wealthiest and most famous people on earth.

Intro: The Promise That Wasn’t

Between 2020 and 2022, a financial frenzy unlike anything the internet had ever seen swept through celebrity mansions, corporate boardrooms, and Reddit forums with equal ferocity. Non-fungible tokens, NFTs, were marketed as the future of art, ownership, and community. They were sold as digital deeds, gateways to exclusive clubs, and once-in-a-generation investment opportunities.

They were, for the overwhelming majority of buyers, worthless.

A 2023 study by dappGambl, which analyzed over 73,000 NFT collections, found that 95% of them held a market cap of zero ETH, meaning they had become entirely valueless. Of the 73,257 collections examined, 69,795 had no measurable value whatsoever. Millions of ordinary people had bought in at the peak of a media-fueled hysteria, often goaded by celebrities who had been paid to promote tokens they would quietly dump the moment the market moved.

This is the story of how it happened, who profited, and who was left holding digital nothing.

Part One: What Is a Rugpull?

In crypto slang, a “rugpull” refers to a scheme in which developers or promoters of a token or NFT project hype up its value, attract buyers, and then abruptly abandon the project, taking investor funds with them. The rug is pulled from beneath the community that trusted them.

Rugpulls operate on a spectrum. At the more brazen end, founders vanish overnight with treasury funds, deleting their Twitter accounts and Discord servers without a word. At the subtler end, and this is where much of the NFT era lived, developers simply stopped delivering on promises, let communities decay, and quietly moved on once they had cashed out their allocations. Both are forms of fraud. Both destroyed wealth. And both were enabled, in large part, by a celebrity and media ecosystem that had every financial incentive to look the other way.

The mechanics were simple: create a collection of algorithmically generated images, often nothing more than a cartoon animal with randomized traits, promise a “roadmap” of utilities, games, exclusive events, and metaverse integrations, get a famous face to tweet about it, watch the floor price spike, and sell. The buyers, left behind in a Discord server full of broken promises, eventually had to reckon with the fact that what they owned was a JPEG with no buyers.

Part Two: The Celebrity Machine

Perhaps no element of the NFT era was more corrosive than the systematic use of celebrity endorsement to legitimize projects that had no substance. Stars across entertainment, sports, and music either launched their own NFT collections or promoted existing ones for undisclosed fees, often without informing their audiences of any financial relationship, a likely violation of FTC disclosure guidelines.

Kim Kardashian was charged by the U.S. Securities and Exchange Commission in 2022 for promoting EthereumMax tokens on her Instagram without disclosing that she had been paid $250,000 to do so. She settled the charges for $1.26 million without admitting or denying wrongdoing. The EthereumMax token had been aggressively promoted around a Floyd Mayweather boxing match and lost the vast majority of its value in the months following the campaign.

Floyd Mayweather Jr. himself faced multiple lawsuits connected to his promotion of NFT and crypto projects. He was named in a class-action lawsuit related to the EthereumMax scheme alongside Kardashian. He had previously faced legal action over his promotion of ICOs during the 2017 crypto boom, and appeared to have learned little from the experience.

Matt Damon starred in a widely aired television commercial for Crypto.com in late 2021, intoning that “fortune favors the brave” over dramatic historical imagery. The timing was almost comically unfortunate: it aired just as the crypto market was approaching its all-time peak. Many who bought in following the campaign lost the majority of their investment within eighteen months.

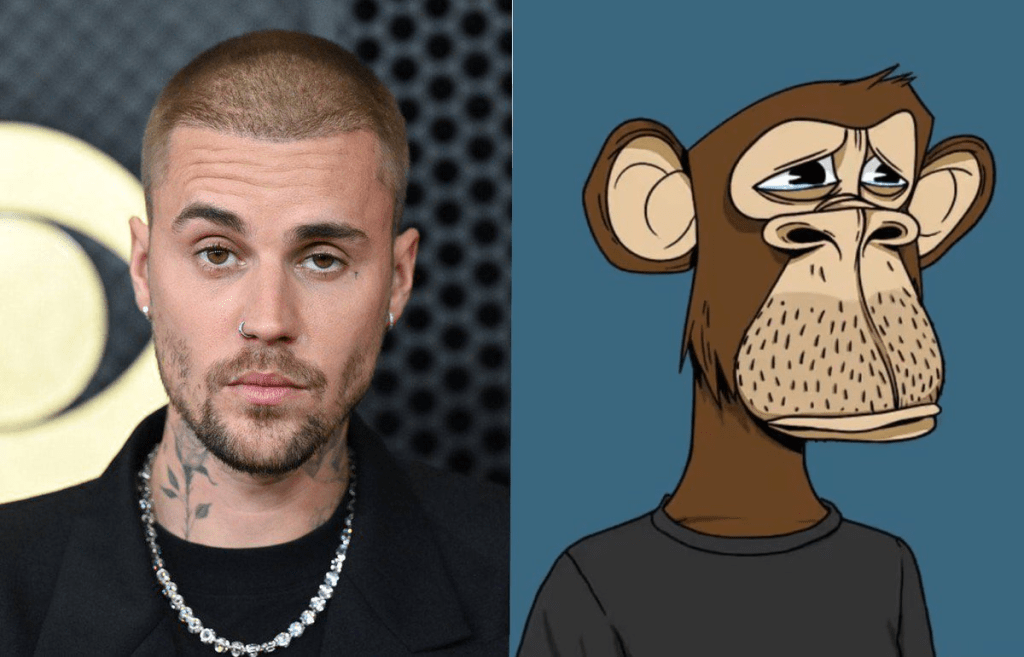

Paris Hilton launched her own NFT collection and partnered with the Bored Ape Yacht Club ecosystem, appearing on The Tonight Show Starring Jimmy Fallon in January 2022 to discuss her Bored Ape. The segment, which critics described as a thinly veiled advertisement, aired during what would prove to be one of the final months of the NFT bubble’s peak. By the following year, Bored Ape floor prices had fallen from peaks of around $429,000 per token to a fraction of that value.

Tom Brady co-founded Autograph, an NFT platform, and attracted athletes and celebrities to the platform including Tiger Woods, Simone Biles, and Derek Jeter. Autograph raised $170 million in funding. By 2023, the platform had quietly shut down, citing “market conditions,” leaving NFT holders with tokens representing a defunct platform.

Justin Bieber purchased a Bored Ape NFT in January 2022 for approximately $1.3 million. He was roundly mocked at the time for overpaying even by the inflated standards of the day. By late 2023, the same token’s estimated value had collapsed by over 95%.

These were not isolated incidents. They represented a coordinated, industry-wide strategy to use fame as a substitute for due diligence. The implicit promise was clear: if someone this rich and connected is involved, it must be legitimate. It was a logic that had powered every financial bubble in history, and it worked again.

Part Three: The Media Amplification Engine

Celebrity endorsements alone could not have sustained the mania. They required a media ecosystem willing, even eager, to amplify the hype without serious scrutiny.

Major outlets largely failed their audiences during the NFT boom. Publications that should have been asking hard questions about utility, fraud risk, and market manipulation instead ran breathless features about the democratization of art and the new creator economy. Business media treated NFT sales figures as straightforward financial news rather than examining the wash trading, in which buyers and sellers are the same entity or collude to inflate apparent prices, that was rampant across major NFT marketplaces.

The launch of the Bored Ape Yacht Club in April 2021 was covered as a genuine cultural phenomenon. Magazines profiled BAYC founders. Feature pieces celebrated celebrity owners. The project’s “roadmap,” promising a metaverse, games, merchandise, and exclusive events, was reported on as though it were a business prospectus rather than a collection of aspirational bullet points on a website.

BAYC’s parent company, Yuga Labs, raised $450 million in a funding round at a $4 billion valuation in March 2022. Weeks later, the NFT market began its precipitous collapse. In 2023, the SEC began investigating Yuga Labs over whether its NFT sales constituted the offering of unregistered securities.

Television was no better. CNBC segments celebrated individual NFT millionaires. Morning shows invited NFT creators on to explain why digital monkey pictures were worth hundreds of thousands of dollars. Late-night hosts bought Bored Apes on air. The critical infrastructure of skepticism, the question of who profits when you lose, was almost entirely absent.

Nyan Cat sold as an NFT for $590,000. A clip of LeBron James dunking sold for $208,000 through NBA Top Shot. Twitter founder Jack Dorsey sold the first-ever tweet as an NFT for $2.9 million. Dorsey’s buyer, entrepreneur Sina Estavi, later attempted to resell it and received a highest bid of $280, a 99.99% decline in value. The media treated the original sale as historic. The resale collapse received a fraction of the attention.

Part Four: The Scale of Destruction

When the numbers are assembled honestly, the NFT era represents one of the largest wealth transfers from ordinary people to insiders and early participants in the history of the internet. If you’re wondering, yes, that is the definition of a Ponzi scheme.

The collapse was swift and brutal. Total NFT market volume fell from a peak of approximately $17 billion in January 2022 to under $1 billion by the end of the year. Individual collections that had traded for hundreds of thousands of dollars became effectively unsellable. Discord servers that had once hummed with thousands of true believers went quiet, or were locked entirely when their moderators disappeared.

The communities built around NFT projects were not incidental to the scheme, they were integral to it. Projects encouraged buyers to evangelize, to tweet their purchases, to change their profile pictures to their tokens. The social identity wrapped around NFT ownership made it psychologically difficult for buyers to acknowledge the warning signs. Selling meant admitting loss; holding meant hoping. The community reinforced the hold.

For many buyers, the losses were not trivial. The NFT market attracted participants from demographics that had historically been excluded from investment opportunities, including younger buyers, international buyers, and communities of color drawn in by promises of wealth creation and financial inclusion. The projects most aggressively marketed to these communities were frequently among the most worthless. The democratization of wealth that was promised delivered, in practice, a democratization of losses.

Conclusion: Accountability? Nah, not around here.

As of this writing, accountability for the NFT era has been piecemeal at best. The SEC has pursued a handful of cases. Several high-profile project founders have faced civil suits. The celebrity promoters who collected fees and moved on have largely escaped serious legal consequence.

The structural conditions that enabled the NFT boom have not fundamentally changed. Social media platforms continue to allow paid promotions without adequate disclosure enforcement. Celebrity influence remains available for purchase. The vocabulary of disruption and democratization can still be deployed to short-circuit critical thinking.

What the NFT era demonstrated, with uncomfortable clarity, is that the technologies enabling digital ownership were real, but the products sold on top of them were, in the overwhelming majority of cases, theater. The art was often generated by algorithm. The roadmaps were fiction. The communities were machinery for maintaining price until the insiders had exited.

The buyers were not, as critics sometimes suggest, simply foolish. They were systematically misled by people who knew better and had every financial incentive to say nothing. That is not a market failure. It is a fraud at scale, and the reckoning, years later, remains unfinished.

Sources and statistical references include the dappGambl 2023 NFT study (73,257 collections analyzed), SEC enforcement actions against Kim Kardashian (2022), class-action litigation records related to EthereumMax, public blockchain data on NFT floor price histories, and contemporaneous financial media coverage from 2021 to 2023.

Further reading:

Leave a comment